Introduction to Blockchain Technology

Line up to meet the latest center court champion, Blockchain.

Of course, blockchain won’t actually be making an appearance at Wimbledon this year but as a metaphor it’s quite fitting with people placing bets on both.

A blockchain is a tamper-proof, shared digital ledger which records transactions in either a public or private network. As it’s distributed to all participants in the network, the ledger makes a permanent record as blocks.

Every block that is confirmed and validated are linked and chained from the beginning of the chain to the latest block – giving it the name blockchain.

Each computer on the network is known as a “node”.

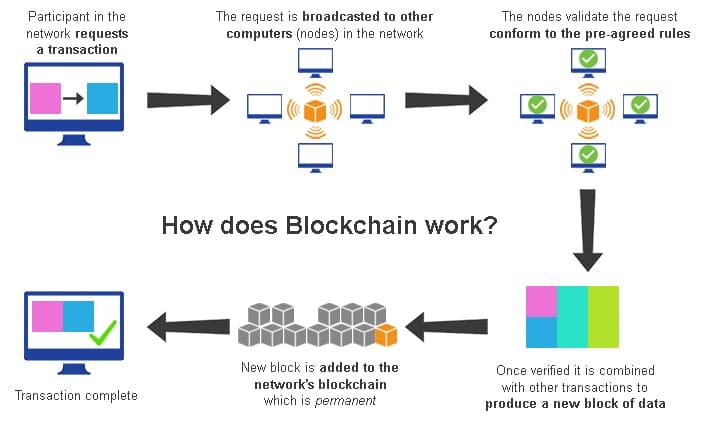

How does a blockchain network work?

Instead of relying on a third party, such as a financial institution, to mediate transactions, participants in a blockchain network use a consensus protocol to agree on ledger content, and cryptographic hashes and digital signatures to ensure the integrity of transactions.

Consensus ensures that the shared ledgers are identical, lowering the risk of fraudulent transactions, because tampering would have to occur across many places at exactly the same time. Cryptographic hashes ensure that any alteration to transaction input — even the smallest of changes — results in a different hash value being generated, which indicates potentially compromised transaction input. Digital signatures ensure that transactions originated from senders (signed with private keys) and not imposters.

The peer-to-peer blockchain network prevents any single participant or group of participants from controlling the underlying infrastructure or system. Participants in the network are all equal, adhering to the same protocols.

At its core, the system records the chronological order of transactions with all agreeing to the validity of transactions using the chosen consensus model. The result is transactions that are irreversible and agreed to by all participants in the network.

Public vs private blockchains

Peer-to-peer: Each “peer” has 100% of the data and any updates are shared amongst the peers. This makes each peer more independent and enables them to continue operating even in the event of losing connectivity to the rest of the network. Peer-to-peer is more robust because there is no central server that can be controlled, making closing down the peer-to-peer network more difficult.

Client server: In a typical office environment, data is held on severs so whenever you log in you can access this data. The servers hold all the data, an example is the internet where websites are held on servers.

What are the business benefits of blockchain?

Blockchain can add value if:

-

- Multiple parties share data and need the same visibility of this data

- Multiple parties update data and require the changes to be recorded

- Participants need to be able to trust the changes that are recorded have been verified as valid

- Intermediaries add cost and complexity

- Interactions are time sensitive, with these delays increasing costs

- Transactions created by participants are dependent on one another

In traditional business networks, all participants maintain their own ledgers with duplication and discrepancies that result in disputes, increased settlement times, and the need for intermediaries with their associated overhead costs.

However, by using blockchain-based shared ledgers, where transactions cannot be changed once validated, businesses can save time and costs while reducing risks. Blockchain technologies promise improved transparency among willing participants, automation, ledger customisation, and improved trust in archiving.

Blockchain consensus mechanisms provide consistent dataset with reduced errors and real-time reference data.

Because no one participating member owns the source of origin for information contained in the shared ledger, blockchain technologies lead to increased trust and integrity in the flow of transaction information among the participants.

Conclusion

Only time will tell how good the predictions are for the blockchain innovation as it rivals alongside the cloud and AI for the, ahem, straight-sets victory.

We can see already that blockchain represents a completely new way of conducting business transactions. Check out our next blog post on the implications of blockchain technology and how it will integrate with accounts receivable.